CHAPTER 7

Inter-generational financial planning and the family home

As the name suggests, inter-generational financial planning ('IFP') aims to treat a family as what it usually really is - a single vertically-integrated economic unit. Most people think across the generations when it comes to their wealth management - and so as financial advisers we do too.

This is particularly the case when it comes to homes. Homes account for 43% of Australian household wealth. What's more, around 70% of Australians live in a home they own themselves (with or without a mortgage). Put simply, homes are critical to the financial aspirations of most people.We see all clients as potential candidates for IFP. We always try to spend a little extra time with all new clients, during which we find out a bit more about the person, their life views and their relationships with friends and family. The purpose is not completely social. Often the extra time reveals important facts, hopes and attitudes that can then be blended into our advice and strategies, making them better than ever.

7.1

The Family Home and Retirement Planning

One of the key benefits of a family home is that its value is exempt from calculations used to determine Centrelink aged pension benefits. In addition, if and when an owner needs to move into an aged care facility, only a portion of the family home is counted in the assets test used to calculate the means-tested components of the accommodation and care costs.

This is often a good reason for older people to retain the family home, even beyond the point when they move into aged care.

7.2

Inheritances

In December 2014, the Grattan Institute published 'The Wealth of Generations.' The research paper can be viewed here. The report contains some very significant findings, including the observation that the wealth of Australians aged between 65 and 74 increased by an average of $200,000 in the eight years to 2014. The wealth of Australians aged between 25 and 34 decreased on average over the same period. This increase was entirely due to the fact that older Australians were more likely to own homes, and more likely to own those homes outright, then their younger counterparts.

Amongst other things, this tells us that there is about to be a very significant transfer of wealth from older Australians to their younger children and grandchildren.

7.3

Inheritances upon death - estate planning and the family home

The first thing to note is that not all family homes are included in a deceased's estate. The entity that is 'the family' is not a legal person. Therefore, 'the family' cannot own an asset. Instead, individual members of a family own the home under some form of co-ownership. By far the most common such form is joint tenancy. Joint tenancy is subject to the principle of survivorship, whereby the remaining joint tenants automatically acquire a deceased person's share of a property upon death. There is nothing left to the estate of the deceased. It is only when there is one surviving owner, at which point the property ceases to be a joint tenancy, that estate planning for the property becomes an issue.

Where a couple own a home as joint tenants, the home will eventually form part of the estate of the second member of the couple to die. This means that most wills for home-owning couples will still contemplate the family home as an asset, if only in the event that the willmaker is predeceased by their partner.

If that sounds complicated, let us explain. It is very common for a married couple to own a home together as joint tenants. If one member of the couple die, for example, the husband, then the wife does not 'inherit' her husband's share of the home. Instead, her husband's 'share' of the house is basically cancelled and the wife is then left as the only surviving owner. It is only when the wife dies that the property will be inherited - and it will be inherited according to her will, not his.

7.4

Capital Gains Tax

Provided that the home was the principal place of residence for deceased person, there is no CGT payable upon the transfer of a property following death. This is the case whether title to the property is transferred to the deceased's beneficiaries or is sold to a third party.

The principal place of residence exemption extends for 6 years after a person vacates a property, provided that they do not claim any other property as the principal place of residence during that period. This means that a family home that was owned by someone who spent up to the last six years of their life living elsewhere, such as with relatives or in care, can usually retain its CGT exempt status.

7.4

Targeting the Inheritance

Sometimes, clients will seek to target particular assets to particular beneficiaries in their will. A common example is where there is an adult child who is disabled and continues to live with their parents into adulthood. In these cases, many parents leave the home to that child, and leave other assets (such as investment assets) to their other beneficiaries.

This targeting it one way in which financial planning can extend beyond generations.

7.5

What to do with the Inheritance?

Once a home has become the subject of a will, ultimately it can be either sold or kept. If kept, it can be used either as a place for the beneficiaries to live or held as an investment. If it is lived in by a beneficiary, then it may become their principal place of residence, in which case it will retain its CGT exempt status into the future.

If the family home is a representative residential property (by which we mean it is likely to achieve the average rate of return for residential property) then retaining it as an investment is often a good financial move. The twenty-year average return on residential Australian property to 31 December 2017 was 10.2%. This return slightly exceeded that for Australian equities over the same period.

Whether a home is kept often depends on the number of beneficiaries who are to share it. As would be expected, where multiple beneficiaries are entitled to a share of the property, it is typically harder to keep the property. The beneficiaries would need to agree to become co-owners, which would in turn require that they each have similar personal financial situations.

Keeping the home is more common where there are fewer beneficiaries. If there is only one beneficiary, then he or she simply makes up their own mind as to whether to keep the property. Where there a few beneficiaries, they may decide to own the property as co-owners. Or, one common alternative is for one beneficiary to 'buy out' one or more of the other beneficiaries. This is discussed in this article by Di Rosa Lawyers, in Adelaide.

7.6

Timing the Inheritance

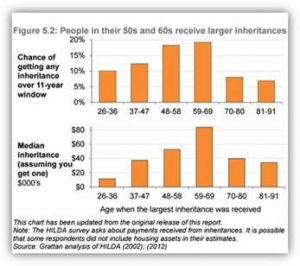

Most inheritances are received relatively later in the recipient's life. The report by the Grattan Institute includes the following graph:

What the graphs show is that a person's prospects of receiving an inheritance peak in that person's 50s and 60s. What's more, if the inheritance is delayed until later in life, it is larger. That is, the relatively few younger people who receive an inheritance receive smaller inheritances.

This would seem to reflect the fact that most people inherit from their parents, which is happening quite late in the inheritors' life as their parents live into their 80s and 90s. (We expect that the more than 5% of inheritors who receive inheritances in their 80s receive them from age-peers such as siblings, or even adult children, rather than parents).

7.7

Assistance Buying Homes That Doesn't Involve Inheritances

Assisting Younger Generations to Buy a Family Home (or a Better Family Home)

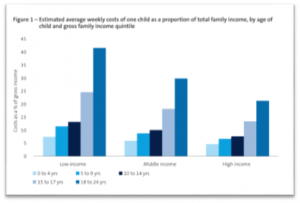

As the above graph makes clear, most inheritances occur after the recipient turns 48. By that age, the recipient is already well into their own peak cost years - the years when they are raising children. The following graph comes from the University of Canberra's National Centre for Social and economic Modelling's (NATSEM) 2013 report, 'The Cost of Raising Children in Australia.'

As this graph shows, the proportion of household income that is spent on children is high throughout their life, peaking once they turn 18. Unfortunately, inheritances, when they come at all, usually come after the kids have been raised.

How handy would an inheritance be if it was received earlier in the recipient's life - when they most need it, but before their benefactor actually dies?

For this reason, increasingly, older clients are looking for ways to assist adult children to buy their own home while the older client is still on the planet. Ways to do this include:

- Buying a home in conjunction with a child;

- Guaranteeing a loan to assist a child to buy his or her own home;

- Utilising multiple interest offset accounts such that the older client's savings can offset the younger person's mortgage;

- The older client gifting some money to the adult child; or

- The older client making a soft loan to the adult child.

Assisting Older Generations to Buy a Family Home (or a Better Family Home)

Sometimes, it is the younger generation that is in a position to help the older generations buy homes. This is often the case where the older generations were the original immigrants to Australia, for example, and arrived with limited employment prospects. The children of immigrants have long been over-represented among the ranks of academic achievers, and this correlates with higher earnings for those children.

In these situations, many of the techniques commonly associated with older clients helping their children can simply be reversed. A younger client might co-own a home with his or her parents, for example. Or, a young person might use their savings to offset a mortgage for their parents.

For higher tax-paying younger clients, the tax advantaged nature of the family home can be of assistance. If the home is wholly-owned by their older relative, with the younger client then to inherit it when their parent or grandparent dies, then there will be no capital gains tax payable when this happens. (Against that is the obvious fact that interest on any money borrowed to finance the purchase is not deductible along the way).

7.8

The Importance of Written Agreements

While most people consider their family to be a single economic unit, the law does not. For that reason, transfers of wealth between generations should usually be supported by written agreements between the participants. This can often be overlooked - especially for social reasons. One very common observation is a son-in-law refusing to sign an agreement that says he must repay money that is lent by his wife's parents.

Persistence is necessary, though, because the absence of a written agreement can mean that the initial intention of the strategy is not met. For example, if a client gives money to another person to be used towards buying a home, then that money becomes the property of that other person. If this other person is married, for example, then the money actually becomes part of the assets of the marriage - and can be distributed accordingly if the marriage ends.

As Ian McLeod of RP Emery puts it:

Verbal agreements are notoriously difficult to prove which makes the enforcement of a verbal agreement time consuming and challenging. Not only do you need to prove the verbal agreement exists (and each of the criterion set out above), but you also need to evidence just what the actual terms of the agreement are, which, in the absence of written documentary evidence, can boil down to one person's word against the other.

7.9

Superannuation and Family Homes

Very commonly, the main focus of IGFP is to provide housing for the younger generations - at least, housing that is within a sensible distance of where Grandma and Grandpa are living.

Accordingly, it pays to remember that, ultimately, private housing must be bought using after-tax dollars. The deposit used to purchase a private residence, for example, must be saved after tax is paid on the purchaser's income. The principal and interest payments on the loan must also be paid out of after-tax income. Ultimately, the whole property is paid for after-tax.

As a result, it becomes clear that, where the tax payable on income is lower, it will require less pre-tax income to buy the same amount of house. The following table shows how much pre-tax income is required to buy a $500,000 property for various marginal tax rates.

| Tax Rate | Pre-Tax Amount Required | Tax Paid | Amount Remaining |

| 0% | $500,000 | 0 | $500,000 |

| 15% | $588,235 | $88,235 | $500,000 |

| 19% | $617,284 | $117,284 | $500,000 |

| 32.5% | $740,741 | $240,741 | $500,000 |

| 37% | $793,651 | $293,651 | $500,000 |

| 45% | $909,091 | $409,091 | $500,000 |

The second column shows the pre-tax cost of a $500,000 property. The 15% tax rate is that rate payable on deductible super contributions into a super fund. The point of the table is this: if families make deductible super contributions into someone's super fund, and then withdraw these contributions tax-free when the relevant person reaches the required age and use the money to purchase housing, the family only needed to earn $588,000 pre-tax to buy a $500,000 property. If the relevant part of the family instead pays tax on income at 45%, and then uses what's left to purchase the property, the $500,000 property costs over $900,000.

Judicious use of super can reduce the cost of a property by more than a third.

Because of this, wherever a property needs to be purchased somewhere within a family structure, it pays to think about whether the tax advantages of super can be realised.

Here is an example of how this might work. Janet is a client in her early sixties. She became a mum at 35 and her only child son Niall is graduating from Uni at the age of 27. Niall wants to save $40,000 over the next three years for use as a home deposit.

Janet's adviser Noni has a good idea. Janet earns $65,000 a year as a senior administrator. Noni suggests that Janet sacrifice an extra $20,000 in salary as a deductible super contribution each year for the next three years. Given her tax rate, this only costs her $13,500 in lost purchasing power each year. She replaces this lost purchasing power by asking Niall to give her $1,100 per month - the money he was intending to save for his deposit.

Within her super fund, Janet accumulates an extra $17,000 each year, after tax. If this is held in a conservative investment (akin to the term deposit), she can expect to have around $52,000 in three years' time. Having reached the age of 65, she can withdraw this amount tax-free and give Niall almost $10,000 more than he would have if he saved the money in his own name.